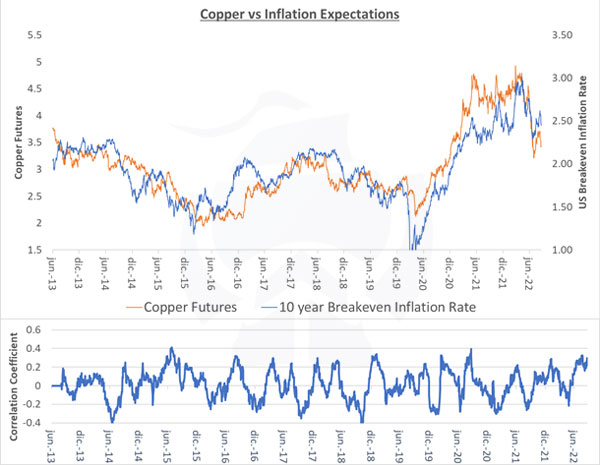

Inflation expectations depend currently on commodities (HG=F). Copper Futures have a strong relationship with inflation breakeven rates and are significantly dropping. This implies that inflation expectations have peaked and will dramatically fall in the short run. As Chinese policy has shifted, the fall in the renminbi is a very significant deflationary pressure for international prices, particularly industrial metals.

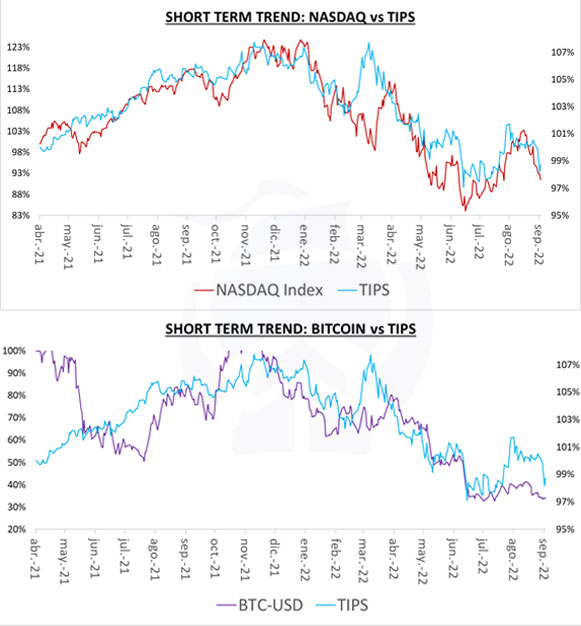

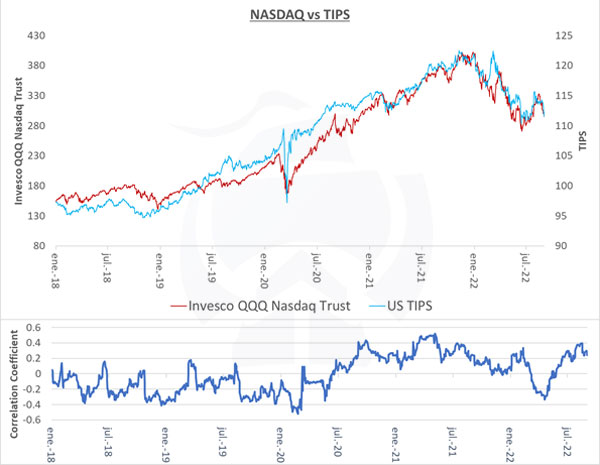

Risk assets are drive currently by real interest rates (TIPS). The correlation and cointegration between the Nasdaq and TIPs point to risk assets depending purely on nominal interest rates, and the Fed’s hawkish rhetoric. With any hint of a chance in stance markets will rally in the short run.

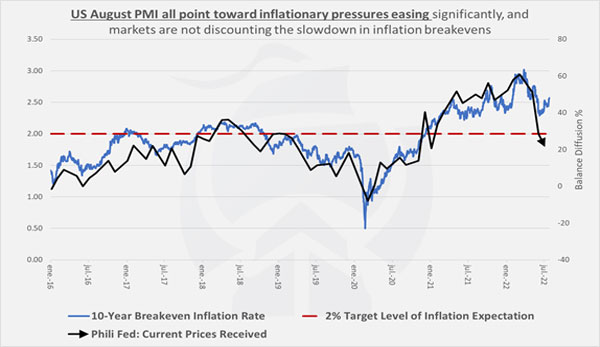

Treasury rates have maxed out, Inflation Expectations are already moderating. All these effects have top inflation expectation (measured by 10Y Breakeven Rates), which implies that Treasury yields have topped. Data for August we believe will confirm the downside risk that exists for inflation. The Fed will start to voice it’s “Win over the Inflation War” in the next quarters.