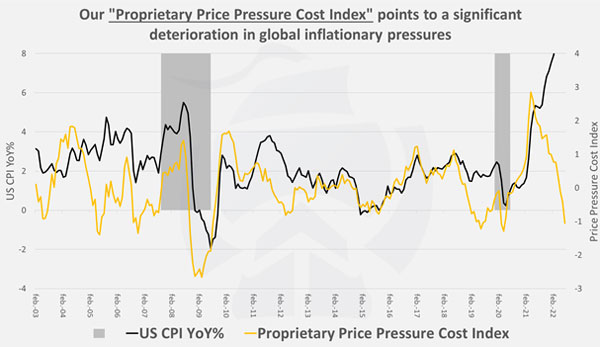

Our Proprietary Price Pressure Cost Index is rolling over rapidly. Our indicator which measures the “rate of acceleration of inflation” and is comprised of data that tends to lead inflation, is rapidly rolling over. This is not only because of base effects in inflation, but also poor international sales expectations, declining lead times and building inventory pressure. This all suggest that inflation expectations should ease going forward.

WOULD LIKE TO KNOW MORE?

Suscribe and receive our monthly market analysis directly to your email.